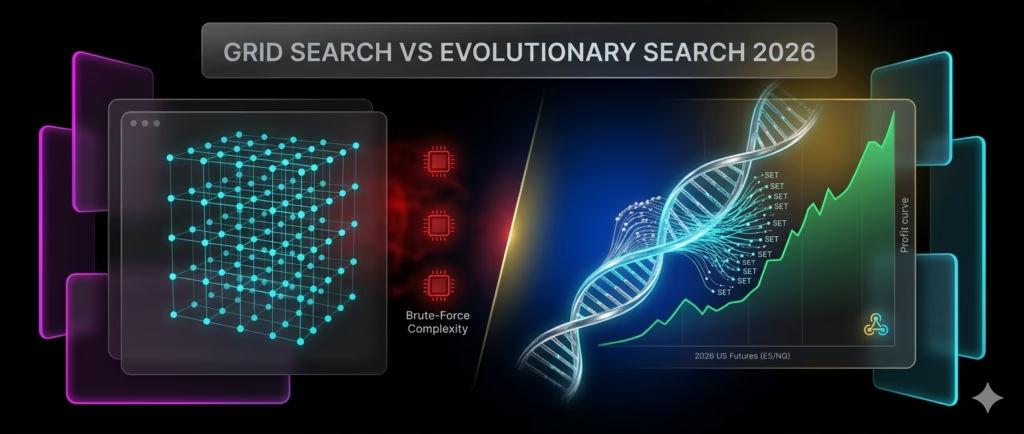

Grid Search vs Evolutionary Search 2026: Optimize Faster

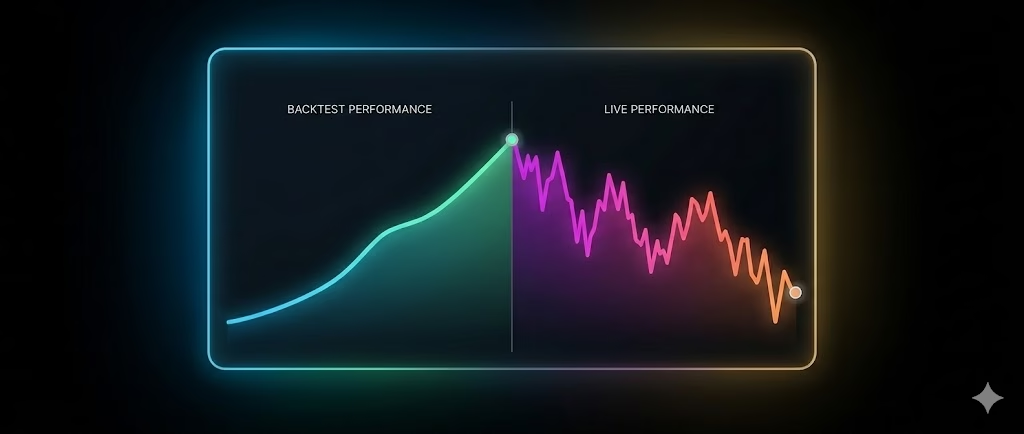

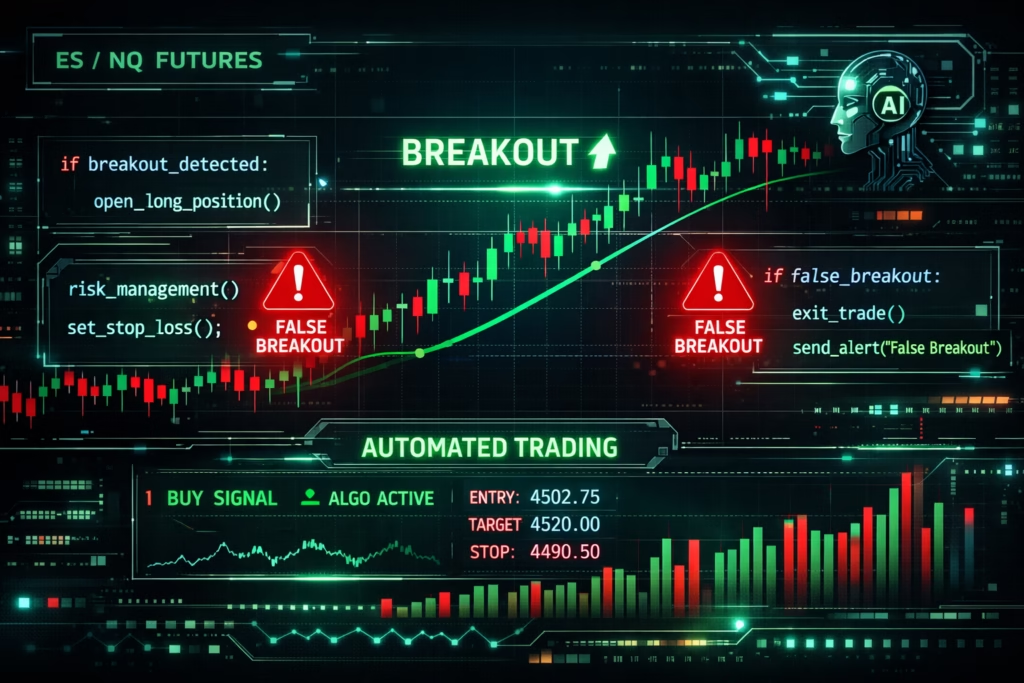

Algo traders waste hours on slow, overfitted parameters. Grid search vs evolutionary search decides who wins in 2026. Grid search brute-forces every combination. Evolutionary search (genetic algorithms and variants) mimics natural selection to evolve smarter solutions. In volatile US futures markets, the wrong choice kills profitability. With 2026 papers proving evolutionary methods outperform on complex […]