Monte Carlo Trading Simulation: Test Strategy Robustness

In the fast-moving world of algorithmic trading, a single backtest can be dangerously misleading. Markets…

In the fast-moving world of algorithmic trading, a single backtest can be dangerously misleading. Markets…

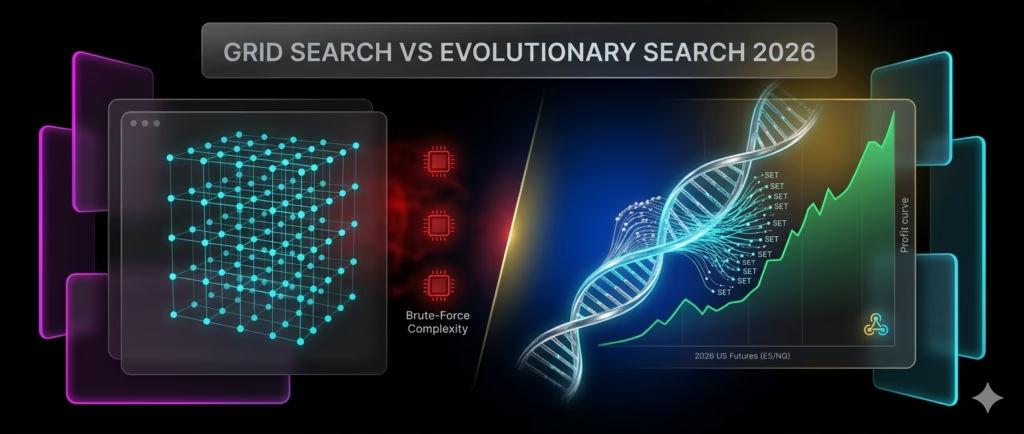

Algo traders waste hours on slow, overfitted parameters. Grid search vs evolutionary search decides who…

In the fast-evolving world of algorithmic trading, Python futures libraries have become essential for building…

Many algorithmic trading strategies exhibit strong performance in historical backtests high returns, favorable win rates,…

The main reasons paper trading (simulation) wins often fail in live trading stem from key…

The Multi-Strategy Portfolio approach has surged in popularity, especially among hedge funds delivering strong returns…

Why a Futures Trading Dashboard Matters in 2026 Futures trading demands real-time visibility, quick decision-making,…

Seasonal trading patterns refer to recurring tendencies in financial markets tied to specific times of…

Introduction: Why Advanced Trading Strategies Matter In today’s competitive trading landscape, success isn’t determined by…

In the fast-paced world of automated trading, downtime isn’t just inconvenient—it’s catastrophic. A single server…