Monte Carlo Trading Simulation: Test Strategy Robustness

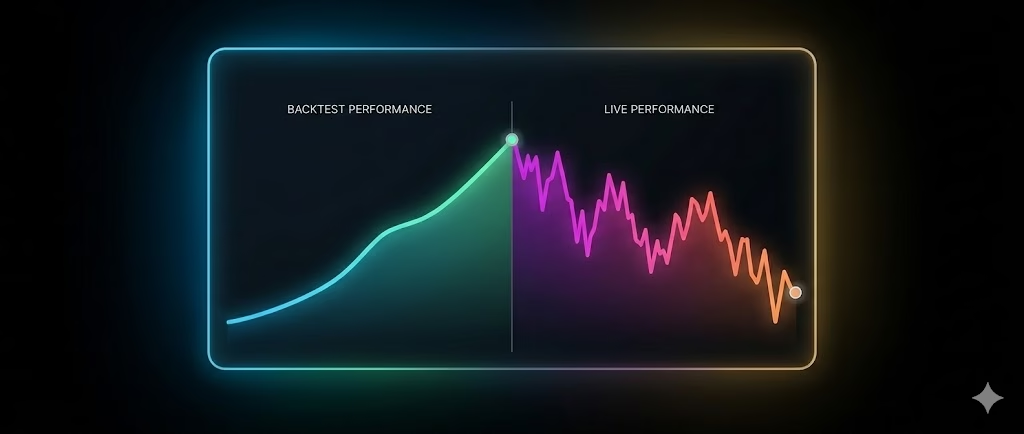

In the fast-moving world of algorithmic trading, a single backtest can be dangerously misleading. Markets…

In the fast-moving world of algorithmic trading, a single backtest can be dangerously misleading. Markets…

In the fast-paced world of algorithmic trading, margin usage is a critical factor that directly…

In today’s ultra-competitive futures markets, timing is everything. High-impact economic releases like Non-Farm Payrolls, FOMC…

Markets don’t move in straight lines — they shift between distinct “regimes” of behavior. One…

In today’s volatile futures markets, relying on a single trading approach often leads to painful…

Algo traders waste hours on slow, overfitted parameters. Grid search vs evolutionary search decides who…

The Institutional Guide to Strategy Validation and Execution Integrity Executive Summary Every algorithmic trader encounters…

Price gaps between related assets still exist in 2026—even in ultra-efficient US markets. Cross market…

A rigorous examination of robustness testing methods for algorithmic trading strategies, drawing on established quantitative…

The prop trading world is consolidating fast. Prop firm mergers and acquisitions are reshaping the…