In the fast-moving world of algorithmic trading, a single backtest can be dangerously misleading. Markets don’t repeat history exactly — they throw curveballs in the form of volatility spikes, regime shifts, and random trade sequences. That’s where monte carlo trading simulation shines as the gold-standard robustness test. By running thousands of randomized scenarios on your strategy’s historical trades, you uncover the true probability of drawdowns, ruin, and long-term profitability before risking real capital.

As of March 2026, monte carlo trading simulation has become even more essential with heightened market volatility in US futures. Professional traders and prop-firm participants now combine it with no-code automation tools to deploy battle-tested strategies live. This updated guide walks you through everything — from basics to 2026 best practices — and shows exactly how to pair it with PickMyTrade for seamless futures automation on US markets.

What Is Monte Carlo Trading Simulation?

Monte carlo trading simulation is a statistical technique that generates thousands of alternative equity curves by injecting controlled randomness into your backtest data. Instead of relying on one historical path, it reshuffles trade order, resamples outcomes with replacement, or adds realistic noise (slippage, volatility shocks) to stress-test performance across thousands of “what-if” futures.

Popular methods include:

- Reshuffle (permutation): Randomly reorder the exact same trades to test sequence dependency.

- Bootstrap/resample: Draw trades randomly with replacement to simulate new distributions.

- Randomized exits or noise infusion: Tweak entry/exit timing or add small random variations to mimic live-market friction.

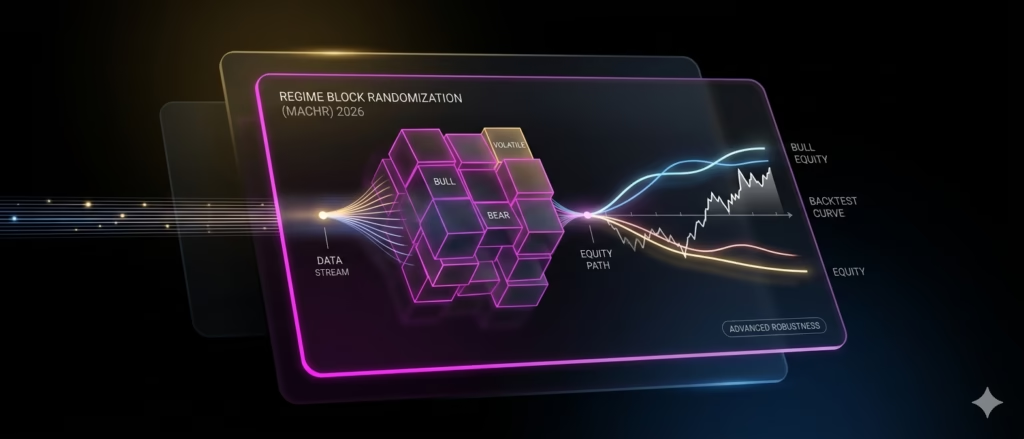

- Regime-aware Monte Carlo (newer 2025–2026 variants): Incorporate market-regime blocks from tools like StrategyQuant.

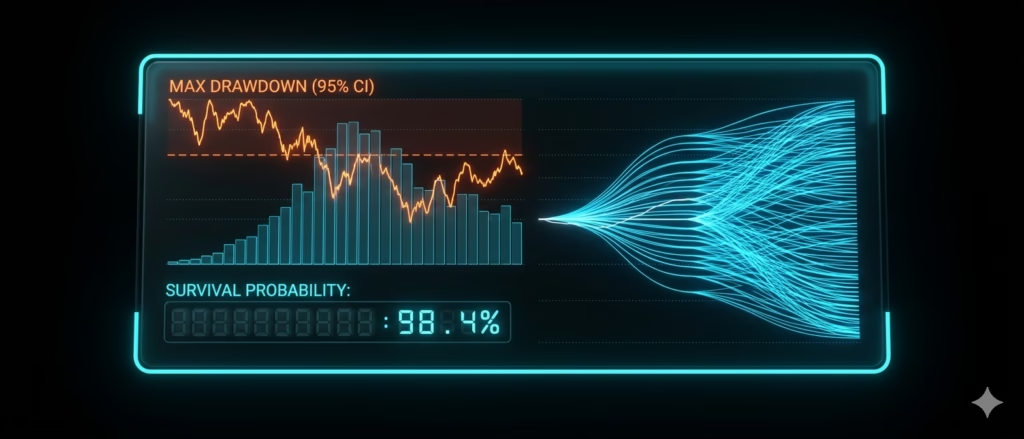

The output? A distribution of outcomes — average return, 95th-percentile drawdown, probability of max drawdown exceeding your risk tolerance, and more. If your strategy survives 1,000+ simulations with consistent metrics, it’s far more likely to hold up live.

Why Monte Carlo Trading Simulation Is Critical for Strategy Robustness Testing

Single-path backtests often overfit to lucky streaks or specific market regimes. Monte carlo trading simulation answers the real questions:

- What’s the realistic worst-case drawdown in 90 % of scenarios?

- Will my strategy survive a sudden volatility spike like we saw in early 2025?

- Is my edge genuine, or just curve-fitting?

Recent 2025–2026 analyses from BuildAlpha, BacktestBase, and NinjaTrader confirm that strategies passing rigorous monte carlo trading simulation show 30–50 % lower live failure rates. In futures markets — where leverage amplifies every slippage — this robustness edge is priceless.

How to Perform a Monte Carlo Trading Simulation (Step-by-Step 2026 Guide)

- Export clean trade data — Include entry/exit prices, P&L, duration, and slippage estimates from your backtester (TradingView, NinjaTrader, or QuantConnect).

- Choose simulation type — Start with 1,000–5,000 runs (1,000 is the 2026 industry minimum for statistical stability).

- Apply randomization — Use Python (pandas + numpy), AmiBroker, StrategyQuant, or free online tools like BacktestBase’s Monte Carlo stress tester (updated January 2026).

- Analyze results — Generate equity-band charts, drawdown histograms, and risk metrics. Look for strategies where median profit factor > 1.5 and 95 % drawdown stays within your capital limits.

- Combine with walk-forward and permutation tests — Modern best practice: never rely on Monte Carlo alone.

Pro tip for 2026: Add “regime block randomization” (MACHR) to test how your strategy behaves when bull-to-bear transitions are shuffled — a feature now standard in advanced platforms.

Click here To Automate TradingView Strategy

Recent Advances in Monte Carlo Trading Simulation (2025–2026)

- Free instant stress testers — BacktestBase now offers one-click Monte Carlo with a 30-point robustness score (Jan 2026 update).

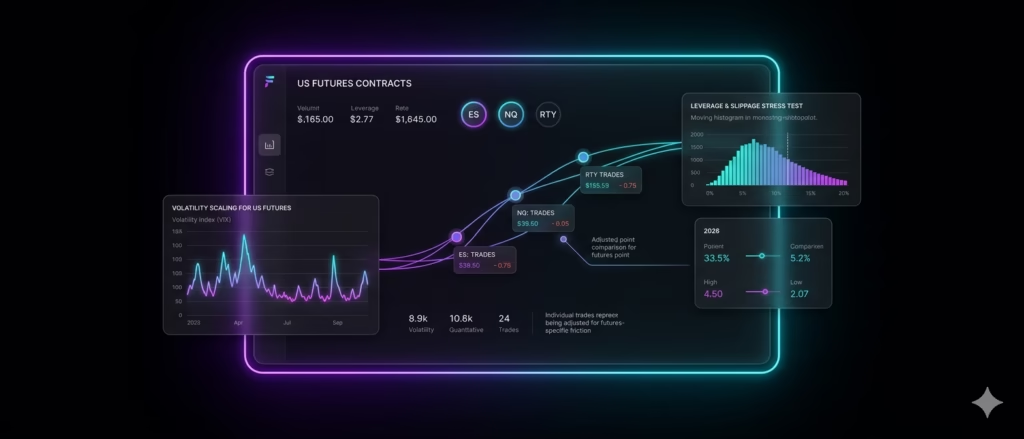

- Futures-specific tools — NinjaTrader’s October 2025 guide highlights Monte Carlo for ES, NQ, and YM contracts, emphasizing volatility scaling.

- AI-enhanced variants — Some platforms now layer latent-regime detection before randomization for more realistic forward paths.

- Integration with automation — The biggest 2026 leap: run monte carlo trading simulation on a strategy, then instantly push the validated signals to live execution.

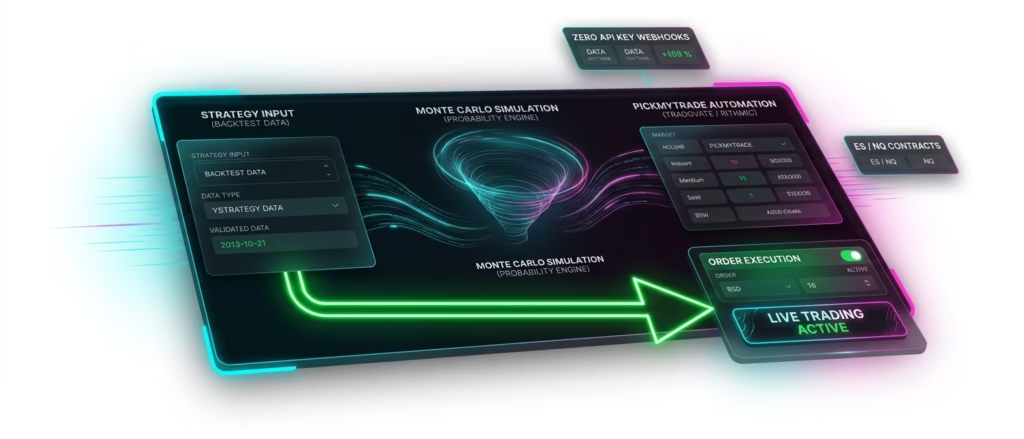

Automate Robust Futures Strategies with PickMyTrade on US Markets

Once your strategy clears monte carlo trading simulation, the next step is live deployment without manual intervention. Enter PickMyTrade — the leading no-code automation platform built specifically for US futures trading.

PickMyTrade connects TradingView alerts directly to Tradovate, Rithmic, Interactive Brokers, and major prop firms via ultra-low-latency webhooks. Key 2026 advantages:

- Unlimited strategies, tickers (ES, NQ, YM, RTY, etc.), and accounts on one $50/month plan.

- Native futures logic with intelligent contract scaling and risk filters.

- 24/7 execution with multi-session automation and prop-firm support (Apex, Blue Guardian, Topstep, and more).

- Zero API keys needed — simply set alerts for buy/sell/close and let PickMyTrade handle the rest.

Workflow: Backtest → Monte carlo trading simulation → Validate robustness → Connect TradingView strategy to PickMyTrade → Automate on live US futures markets with built-in risk automation. Traders report 20–40 % fewer execution errors and seamless scaling across multiple prop accounts.

Common Pitfalls to Avoid in 2026

- Relying only on average results (always check 5th/95th percentiles).

- Using unrealistic slippage or zero commissions.

- Running too few simulations (<500).

- Ignoring regime shifts — always layer block randomization.

- Deploying without forward-testing the automated version on PickMyTrade’s demo.

Conclusion: Make Monte Carlo Trading Simulation Your 2026 Edge

Backtests lie. Monte carlo trading simulation reveals the truth. By stress-testing thousands of randomized futures, you build strategies that survive real markets — then automate them effortlessly with PickMyTrade on US futures. Whether you trade ES/NQ scalps or longer-term momentum setups, this combination of statistical rigor and no-code execution is the professional standard in 2026.

Ready to bulletproof your edge? Export your latest strategy, run a monte carlo trading simulation today, and connect the winners to PickMyTrade. Your future equity curve will thank you.

Most Asked FAQs

What is Monte Carlo trading simulation exactly?

It’s a statistical robustness test that runs 1,000–5,000 randomized versions of your historical trades (reshuffling order, resampling, or adding noise) to show the full range of possible outcomes instead of one backtest path.

How many simulations should I run?

1,000 is the 2026 minimum for reliable statistics; 5,000+ is ideal for high-confidence drawdown percentiles.

Does Monte Carlo trading simulation guarantee my strategy will profit?

No. It estimates risk ranges and detects overfitting. A passing test means higher probability of robustness — never a guarantee.

What’s the difference between reshuffle and resample Monte Carlo?

Reshuffle keeps the exact trade list but changes sequence (tests path dependency). Resample draws trades with replacement, creating new statistical distributions for broader stress testing.

Can I use Monte Carlo trading simulation with PickMyTrade?

Absolutely. Validate your TradingView strategy first with Monte Carlo, then connect alerts to PickMyTrade for instant 24/7 automation on Tradovate or Rithmic US futures accounts.

Disclaimer:

This content is for informational purposes only and does not constitute financial, investment, or trading advice. Trading and investing in financial markets involve risk, and it is possible to lose some or all of your capital. Always perform your own research and consult with a licensed financial advisor before making any trading decisions. The mention of any proprietary trading firms, brokers, does not constitute an endorsement or partnership. Ensure you understand all terms, conditions, and compliance requirements of the firms and platforms you use.

Also Checkout: Connect Tradovate with Trading view using PickMyTrade